You will be aware that Treasury is now looking at support for SMEs who pay themselves via dividend income. They tweeted as such themselves this morning.

We’re delighted that the Treasury is urgently looking at ways to

help business owners who pay themselves via dividend income, according to their

own Twitter account this morning where they say they are ‘looking at

proposals’.

At the moment these smaller businesses, often one-person limited

companies, feel as though they have been forgotten.

We have been in contact with the Treasury to share our research with

SMEs conducted in recent weeks and have suggested a practical solution that

would be in line with measures put in place for the employed and larger

businesses.

We suggest the government looks at extending the Self-Employment

Income Support Scheme (SEISS) to include salary and dividend income from

owner-managed companies, as well as self-employment income, but to exclude any

furlough grants received.

This measure would bring support for those affected in line with the

support being provided to unincorporated businesses and employees.

This would be fair and equitable, and in fact would improve on SEISS

by eliminating double counting where individuals have a mixture of employment

and self-employment.

Over the course of the past few

weeks, UK200 Group, of which we are members, has been conducting research

amongst small businesses across South East and the UK.

The results make for worrying

reading with more than 40% of SMEs closed as a result of the lockdown and more

than half of all SMEs businesses having furloughed staff.

There has been so much reported

in the press about the financial impact of the lockdown due to Coronavirus.

Whilst the government is doing much to support businesses and the economy, the

reality is that not all businesses or jobs will be saved. Rishi Sunak has

said this himself.

Our research really brings home the reality for

many businesses. We are sharing some of the comments SMEs made to us in

the research. So, in their own words, this is what it means to SMEs in

South East:

After nearly 2 weeks,

the bank has not called me back and even though I’ve gone back to them,

the response is they have my details but they are exceptionally busy and

will get back to me ASAP.

We have contacted our

bank for a loan (in March) but they have been too busy to get back to us.

We know that some farm

machinery dealers in other parts of the country have already been awarded

Local authority grants as we retail machinery and parts, but we cannot get

any answers from West Berkshire Council currently.

We did not get the

interruption loan as Lloyds said we had too much security available so got

a commercial loan – not what we wanted!!

I was employed until

June 19 but am now self-employed so I not eligible for either the support

schemes for the self-employed or the furlough scheme as an employee.

As a small company only

founded 3yrs ago, we will be hit hard in the months to come. We provide

legal services on a consultancy basis, but as most law firms have had to

dramatically reduce operation and in many cases furlough/make

redundancies, our work has rapidly dried up. Our profits were due to fall

in any event and are unpredictable as best. We are suffering simply due to

the fact we have worked exceptionally hard & had two good years

profit. It seems unjust that we receive little to no support, and in the

medium to long term, it makes little sense for the economy for a small

business such as ours to face closure.

l run a B&B but

because l pay council tax and not business rates l am not entitled to the

grant.

I am an owner/director

with my wage topped up by dividends. Thus, no help from the government.

We are a registered dog

homing charity. We have had to suspend rehoming as it involves

non-essential travel. Our charity shop has closed, and we are unable to

continue our fundraising. We are surviving because our trustees are

funding the shortfall, but this cannot continue for more than a few

months. We have to pay remaining staff at the kennels, animal food and

kennel maintenance, services etc. Also, vet fees of £10,000 a month.

The Government has come

up with some good ideas, but the detail is useless. Small firms are being

penalised with no support available often as a result of a technicality.

Home based businesses who pay domestic rates or small companies who rent

premises do not meet the needs of the small business grant mismanaged by

Councils.

Commenting on the survey and the specific examples

from SMEs, a fellow member of UK200 Group said; “Hearing how some businesses

are being affected is heart-breaking. Many of the SMEs we are talking to

feel they have been forgotten. 31% of them are predicting their business

will fail if the lockdown continues beyond the end of June. As yet we

don’t know the likely impact of any ongoing measures once the lockdown is

‘eased’ but this will have a significant and long-lasting impact in the South

East.

We have written to the Prime Minister, the

Chancellor, Tim Loughton, MP for East Worthing and Shoreham and Sir Peter

Bottomley, MP for Worthing West to ask them to prioritise support to Stay

Focused; Protect the Economy and Save Jobs. We are committed to doing

our bit to support our clients and all SMEs by raising issues with the

government on their behalf and by collaborating with the government and others

to achieve these goals.

The

responses to this survey confirm the widely held view that SMEs have been

dramatically impacted by the effect of the pandemic. A total of 1,793

respondents, 42% report that they have closed their business as a result of the

lockdown. A full 88% of respondents have had to scale down operations or close.

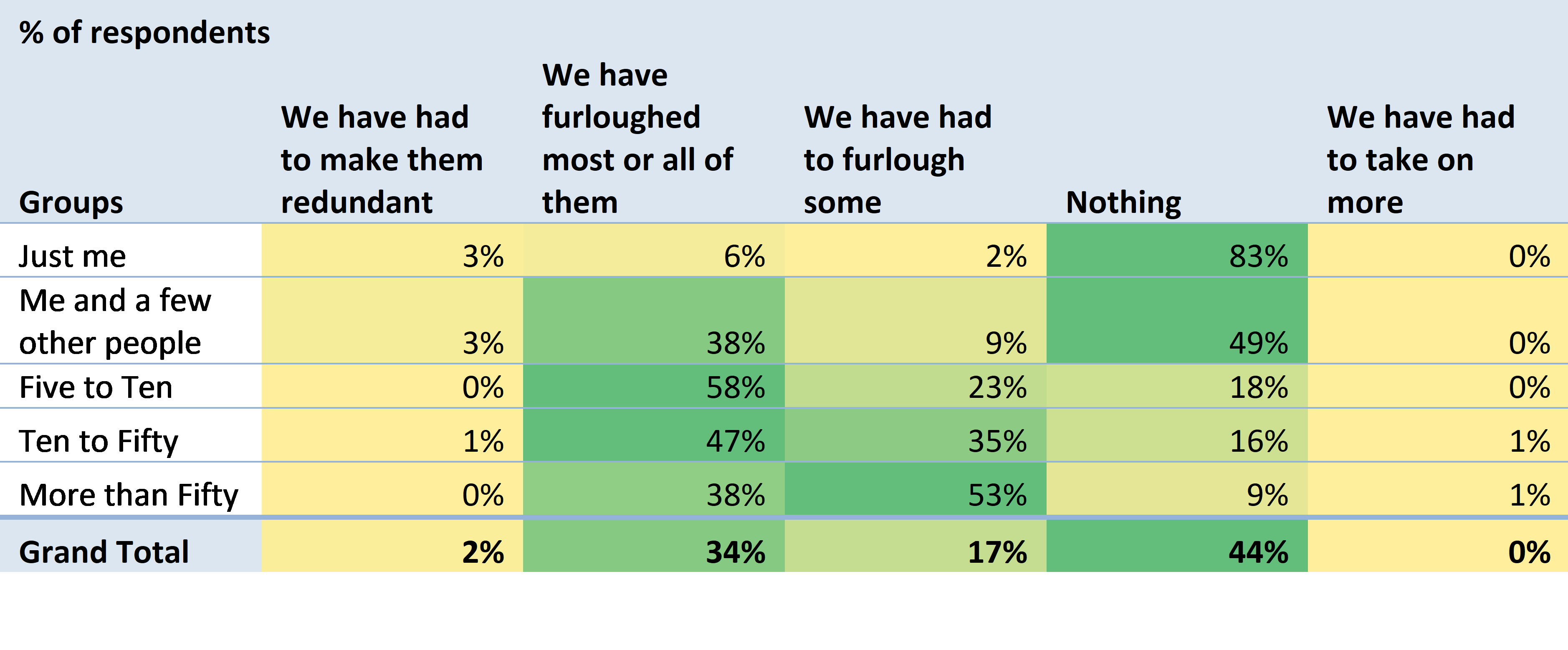

52%

of respondents have furloughed some or all of their employees. Only the smallest

businesses have had to make their staff redundant, with 2% of respondents

having done so. Recruitment is frozen across the board. There is stratification

between businesses of different sizes here; the larger businesses are making

much more use of the furlough scheme than the smaller businesses (comparing

businesses of 5-50+ people to those of 2-5 people).

The

outlook shared by respondents in bleak. If the lockdown extends to 30 June, 73%

of respondents expect to scale down or close (17% expect to close permanently).

Again, we see that bigger businesses expect to be more resilient; 1 in 5 of

those with fewer than 10 people expect to close permanently. If the lockdown

goes beyond 30 June, a full 31% expect to close permanently, while bigger

businesses again appear to feel most resilient as a smaller (but significant)

24% of businesses of >10 people expect to close permanently.

Despite

this outlook, 71% of respondents have not approached the banks for support.

Why? We can only speculate in terms of this survey. Is there no confidence in

future performance to take on debt? Of the businesses who have approached the

banks, 66% have had problems or have been refused funding. Bigger businesses

see a greater proportion approaching the banks, with 56% of >50 people

businesses having done so (vs 29% overall). There is a different experience

felt by different business sizes; of applicants to the banks, 71% of applicants

of 2-10 people have experienced difficulty, vs a smaller 44% of >50 people

applicants.

The respondents are almost united in the impact they have felt from the lockdown, and their pessimistic outlook for the coming months and beyond. The furlough scheme has certainly been accessed, while bank support is interestingly much less accessed. We see different experiences of business sizes throughout the responses.

Overview of dataset

A

total of 1,793 respondents submitted the survey.

Of

these, 68% (1,214) classified themselves as limited companies. Sole traders

accounted for 19%, Partnerships 10%, and the remainder “Other”. The responses

are most representative of limited companies.

60%

(1,073) of respondents are businesses with fewer than 5 people. By business

type, 91% of sole traders reported fewer than 5 people, while 52% of companies

report fewer than 5. Of companies, 41% (494) have between 5 and 50 people, with

7% (88) reporting >50 people. All business sizes are reasonably represented.

92%

(1,758) of respondents are based in England, which follows for each entity

type. 35% of all respondents are from London and the South East, with a further

28% from the north of England. Wales returned 111 respondents, Northern Ireland

15, Scotland 10.

Business performance

92%

(1,648) of respondents reported that business was as expected or better prior

to lockdown. Within the regions this is born out.

40% (724) report this time of year as busy as the rest of the year, with a further 53% (957) reporting it as their very busy period. This is reflected across all business types and regions.

Lockdown impact

A full 42% (746) of

respondents have closed their business as a result. [22%

due to government instruction, 20% due to business falling to nothing]. 38% of

limited companies (467) report closure, vs 53% of sole traders (178).

47%

(833) of respondents are running but with reduced trade volumes, therefore a full 88% of respondents have been

negatively impacted by the lockdown (12% carry on as normal or better).

There

is a stratification between business sizes. Larger entities (>50 people)

have fared better but still we see 29% (33) of this group reporting that they

have closed. A larger 20% of this group (22) report business being the same or

better (vs 12% of the full dataset).

Regionally,

London and SE fares best with 36% (229) reporting closure vs the population’s

42%. Overall, negatively impacted businesses in London and the SE is the same

as the population, at 88%.

Wales

appears to be the worst hit region, with 52% (58) reporting closure. Scotland

reports the same, but the sample size is too small to be reported.

Employees

52%

of respondents (924) have furloughed some or all of their employees. This rises

to 60% (734) of limited companies. Only

2% of businesses (33) have made their staff redundant, and these have been the

smallest businesses (31 of them fewer than 5 people). Does this indicate

the furlough scheme is being used for its intended purpose?

6

businesses in total report having taken on more staff. Recruitment is frozen.

Across

business sizes, there is stratification. Of the smallest (2-5 people), 48%

(292) have furloughed some or all, but of businesses with 5-50 people, 82%

(207) have furloughed some or all employees.

In the >50 people group, this rises to 90% (101). The biggest businesses are the ones most likely to have made use of the furlough scheme.

Table 1 – What

have you done about your staff? [By number of people]

Continued lockdown to 30 June

If

the lockdown continues to 30 June, 17% (312) of businesses expect to close

permanently, a further 19% expect to close temporarily (346), and 36% (649)

expect not to close but to scale down their operations further. In total

therefore, 73% expect to scale down or

close (1,307).

For

all businesses with >10 people, a lower proportion of 12% (55) expect to

close permanently but a larger 50% (232) expect not to close but to scale down

operations.

For respondents with businesses of <10 people, 1 in 5 (257) expect to close permanently.

Continued lockdown beyond 30 June

The

view becomes more pessimistic as 31% of all respondents (558) expect to close

permanently. 82% in total expect to scale down or close (1,465).

For

all businesses with >10 people, now 24% (110) expect to close permanently.

More bigger businesses expect to ride out the storm without closure.

No regional findings to note in either of these cases.

Emerging from lockdown

58%

(1,036) of respondents expect a slow start that is hard to predict, while a

further 27% (488) agree that the restart will be slow, but that normality will

return. Therefore 85% of respondents (1,524) expect slow beginnings. The

largest businesses (>50 people) are more bullish where 40% (45) expect a

slow start but a return to normality.

29%

(522) are concerned their business will not survive the effect of the crisis,

while a further 53% (950) expect to survive but “this year is a write off”.

This generally follows for business sizes, but those with >50 people feel most resilient. Only 13% (14) are concerned they won’t survive and 1 in 5 (22) in this group expect the year to turn out as normal, vs 16% for all our business sizes (264).

Support from the banks

Interestingly, despite the pessimistic outlook presented

above, 71% of respondents (1,273) have

not approached the banks for support. This raises further questions. Is

this due to confidence in liquidity, despite the concerns for longevity

presented? Is it an indicator that businesses are reluctant to take on debt

with no confidence in future profitability (“this year is a write off”)? These

can’t be answered here.

Of

the remaining 28% [NB, rounding] who have approached the banks for funding, 1

in 5 (100) have found them to be very helpful and a further 14% (70) have

received the funding they need. 66% (323)

of those who have approached the banks, have had problems or have been refused

funding.

Of

businesses with 10-50 people, 41% (142) have approached the banks while 56% of

the >50 people businesses (63) have done so. Bigger businesses appear to be

more comfortable/savvy/have felt the need to approach the banks.

In

the >50 people group of those who approach the banks, only 44% (28) of

applicants have had trouble getting the funding they need. Conversely, of

businesses of 2-10 people who have approached the banks, 71% (156) have

experienced trouble.

As perhaps expected, the biggest businesses appear to be finding it the easiest to get access to lending.

About the survey and the data

The

survey was undertaken by the UK200Group the UK’s leading membership association

of independent, quality assured chartered accountancy and law firms. We are one

of the member firms.

Responses were captured in the first 3 weeks of

April 2020. 1,793 SME businesses from across the UK participated in the survey.

SMEs

are the backbone of our economy. They account for 16.7 million of our

workforce. They are vital to the wellbeing of our country and

communities.

That’s

why we recently conducted research amongst the SME community. 1,793

participated and the results of the survey [link] are now being used by us to

call on government for more support for SMEs.

We

wrote to Boris Johnson and Rishi Sunak just last week calling for additional

support for SMEs and we are delighted to see that a 100% government backed loan

has now been introduced.

But

we also know this is not enough in itself. More support and more measures

are needed; we know that many businesses need to see an end to the lockdown but

are worried about the impact on any ongoing social distancing measures.

That’s

why we will keep lobbying the government on behalf of SMEs. Please do

keep telling us what you need so in turn we can do our bit to help you.

In

the past few weeks we’ve been calling on the government to provide further

support for SMEs. We’re delighted that today the government has announced

a 100% government backed loan facility for SMEs to borrow up to £50,000.

Our view on the new scheme is that this is just the type of funding that is required and complements the main CBILS scheme very well. The simplified application should help to streamline the application process and the ability to defer capital repayments for 12 months provides business owners the time to re-structure their business and the confidence to accept the loan. Where the decision for Banks lending to a business was marginal, delays and rejections were likely, but this scheme will be a game changer for some businesses.

The impact from the Coronavirus has been far-reaching and over the past few weeks has changed the way we live for the past few weeks, no matter where you are in the world. In the UK, the last few weeks have most definitely been a challenge for most, if not all, businesses.

The Chancellor has been keen to point out that he is doing everything he can to limit the number of business failures during this period of uncertainty. From providing the opportunity for businesses to furlough workers and receive a grant for their wages from the Government to agreeing deferrals, payment holidays, and providing cash for loans and grants. It does feel like there has been an attempt to support businesses, all for a period of at least three months. At the same time, the Chancellor has told us that there will be dark days ahead.

Starting Back Up Again

The Government are keen to start the economy moving again although the lockdown is set to continue until at least 7 May 2020. Most businesses have focused on their immediate cash requirements over the last few weeks, using short term cash flow forecasts to understand the actual cash coming in and what is going out. Using these forecasts as a base, businesses should now be starting to look at what the next few months will look like. We look at some actions that you can take below:

1. Speak to Your Existing Customer Base

Speaking to your customers will help you to understand what their challenges are, what their immediate/short-term needs look like and will help you to assess their ability to pay you going forwards. There may need to be some adjustments to orders received based on how they envisage demand after the lockdown comes to an end.

2. Turning Work in Progress into Cash

Whether you are a professional services firm or a manufacturing business, reviewing your work in progress will help you to understand whether you have the ability to complete any of your existing work in progress without the need for additional purchases or input. Concentrating some of your initial efforts on turning work in progress into cash will assist you with your working capital cycle.

3. Identify What Additional Purchases You Need

Carrying out a review of your work in progress will also help you identify what purchases you need to make in order to complete your existing orders. Where you have outstanding payments to suppliers, talking to them about the orders that you have received and cashflow will help you to work with your suppliers to get moving again.

4. Book Your Haulage in Advance

If you use an outsourced logistics or distribution operation, make sure that you have booked your haulage in advance so that any delays in getting finished products out to your customers are minimised.

5. Reviewing Your Supply Chain

This is a good opportunity to speak to suppliers and understand what their challenges are. Building relationships with your suppliers will go a good way to helping you to move forward – if you have communicated with them with regards to your challenges, the chances are they will be more amenable to being flexible on payment terms in the short term.

6. Consider What the Return to Work Looks Like for Your Employees

Where you have furloughed staff, take some time to think about whether a return to work needs to be phased or shift patterns need to be changed if social distancing rules are set to continue. Where working patterns need to be changed, make sure you seek advice from your employment advisors.

Looking Further Ahead

The position now may seem

relatively stable, but the VAT, tax and loan payments which have been deferred

will all need to be paid back at some point. Making sure you have enough cash in

the future months to meet these obligations will be vital if your business is

to exit this period relatively unscathed. Cash will be tight whilst the working

capital cycle builds up again and there is likely to be some flex needed with

payment terms. Starting to prepare a longer-term cashflow forecast will help

you to understand what additional funding requirements you may need, and in

what form.

Many businesses are likely to need some additional help as they start back up

again. Even businesses which have been going for many years will likely need to

treat their business as a start-up for the next few months. Taking action now

will ensure that the dark days ahead will end sooner rather than later. If you

are concerned about what the future holds for your business or need some advice

about what steps you should be taking next, please get in touch with our team

who will be able to help you.

Once you’ve claimed, you’ll get a claim reference number.

HMRC will then check that your claim is correct and pay the claim amount by

Bacs into your bank account within 6 working days.

You must:

keep a copy of the claim reference number for your records

keep a copy of your calculations in case HMRC need more information about your claim

tell your employees that you have made a claim and that they do not need to take any more action

pay your employee their wages, if you have not already

Contacting HMRC

We are receiving very high numbers of calls. Contacting HMRC

unnecessarily puts our essential public services at risk during these

challenging times.

Do not contact HMRC unless it has been more than 10 working

days since you made the claim and you have not received it in that time.

New research has revealed that 25.8% of struggling small businesses in the South East do not believe their business will survive the Coronavirus crisis. This compares to 30% across the UK.

Additionally,

the research which has been conducted with 1,400 small businesses across the UK

shows that 80% of businesses who feel they are at risk of failing are

encountering problems in getting help from the banks.

The research, which has been undertaken by The Martlet Partnership together with other members of the UK200Group, asked small businesses across the UK to share information about how their business was faring before the lockdown and what has happened since.

92% of the

businesses surveyed felt their business was either trading ‘as expected’ or

‘better than expected’ before the crisis. Since the lockdown 40% of these

businesses have closed, either by the government or due to falling trade.

But the

biggest underlying concern for many is the inability to access funds.

Many

participating in the survey recognise that the banks are doing their best, but

they are stretched and are struggling due to a combination of lack of clarity

on the new schemes from the government, increased demand and reduced resources

due to the lockdown.

One

respondent, an optician commented; “After nearly 2 weeks, the bank has not

called me back and even though I’ve gone back to them, the response is they

have my details, but they are exceptionally busy and will get back to me ASAP.”

The issue is

compounded due to grants to cover furloughed staff costs not yet being

available and thus the pressure on the cashflow for these small businesses is

being stretched to breaking point.

Commenting managing director, David Macdonald of The Martlet Partnership of said; “Our concern is that these small businesses will simply run out of cash and that will result in many very good small businesses failing. Yet this is avoidable as there are grants and schemes that have been made available, but they are not easily accessible or understood. We are working with clients to support them in packaging their applications and then presenting them to the banks to ensure they have the best chance of a quick and positive response and thus can get the money they need to survive.”

We urge all

small business owners to ask their accountants and business advisers to help

them with their grant and loan applications. Aside from being able to

support you with your applications, they can also clearly explain the different

options and schemes available and can advise businesses on the best course of

action for them.

The online portal through which businesses can register their furloughed workers and apply to receive a grant to cover 80% of furloughed workers wages from the government, will be available from 20th April.

Furthermore, the government has extended the eligibility to 19 March

2020 – the day before the scheme was announced. Previously the date had been

set as 28th February.

This means that employers can claim for

furloughed employees that were employed and on their PAYE payroll on or before

19 March 2020.

Clearly

getting details of the date from when employers can start making a claim plus

the date extension is welcome news.

However, it seems clear that the HMRC will be inundated with queries and

claims as soon as their online portal opens on 20th April.

Therefore,

they have asked accountants such as us, to support them in this mammoth task of

getting these grants to businesses as quickly as possible and with the minimum

of fuss.

If you need to

apply for a grant, we recommend that you start to collate the information that

you will need now, ready to submit your application on 20th April to

receive your grant at the earliest possible date.

The key things

that employers will need to make a claim are:

Your PAYE reference number, UTR and Company number (if applicable)

The number of employees being furloughed

The claim period (start and end date)

Amount claimed

Your bank account number and sort code

Your contact name and your phone number

N.B. In

most cases, Payroll agents are unable to file a claim on behalf of an

employer. Unless you can confirm that your agent can definitely do so,

you will need to be registered for PAYE Online through the Government Gateway.

If you would like assistance with

making your claim, please get in touch at the earliest opportunity. Even if we

cannot make the claim on your behalf, we will help you gather the required

information and submit it in the correct format to help you get the funds as

quickly as possible.